As

Elon Musk's

SpaceX moves closer to what could become one of the biggest stock market debuts in history, opposition to the company's proposed public offering is beginning to grow. In recent weeks, a major Danish pension fund, senior public investment officials in the United States and one of America's largest teachers' unions have all raised concerns about the governance structure of the rocket company and the level of control Musk is expected to retain after the IPO.

AkademikerPension, one of Denmark's largest pension funds with about $25 billion in assets under management, has announced that it will boycott the SpaceX IPO. According to Bloomberg, the fund has blacklisted the company stating that SpaceX is "grossly overvalued". The fund said it would avoid investing even if the valuation were lower because of concerns about shareholder rights and accountability. Earlier this month, New York City Comptroller Mark Levine joined New York State Comptroller Thomas P. DiNapoli and California Public Employees' Retirement System CEO Marcie Frost in sending a letter to SpaceX executives. Together, the three institutions oversee more than $1 trillion in assets on behalf of millions of public workers, including teachers, firefighters, police officers and nurses. In the letter, the investors warned that the governance structure reportedly planned for SpaceX could weaken transparency and limit shareholder protections.

Levine said there were "many glaring governance red flags including a lack of genuine checks and balances for Elon Musk as CEO," while DiNapoli said the structure could leave shareholders with "virtually no recourse" over how the company conducts business.

The concerns have now spread beyond investment groups. Randi Weingarten, president of the American Federation of Teachers (AFT), recently wrote to the US Securities and Exchange Commission (SEC), urging regulators to closely examine SpaceX's governance framework before the company begins trading publicly. Together, the objections signal that while investor interest in SpaceX remains strong, questions about governance, accountability and shareholder rights are emerging as a key issue ahead of the company's highly anticipated IPO.

Danish pension fund blacklists SpaceX IPO

According to a report by Bloomberg, AkademikerPension, which manages $25 billion in assets, has blacklisted the aerospace giant despite its massive target valuation of at least $1.8 trillion. Anders Schelde, the fund’s chief investment officer, stated in an email that SpaceX is not only grossly overvalued but is also hindered by a catastrophic governance structure. He emphasized that even if the financial valuation were reasonable, the fund would still feel compelled to exclude SpaceX from its portfolio. This decision stems from the expectation that Musk will command roughly 80% of the company's voting rights while simultaneously acting as chief executive, chief technology officer, and chairman of the board.

According to AkademikerPension’s independent calculations, SpaceX cannot reasonably exceed a valuation of $1 trillion, leading Schelde to conclude that the fund could not justify participating in the IPO from an investment-return perspective. The fund warned that investors are effectively being asked to accept an unprecedentedly low risk premium for a highly uncertain company where pricing appears to be driven more by Musk’s narratives than by actual economic realities.

Schelde clarified that the decision is not a reflection of the quality of SpaceX's technology or engineering expertise, noting that the fund would otherwise like to invest in its innovations if the valuation and governance risks were mitigated.

NYC Comptroller Mark Levine's letter to Elon Musk

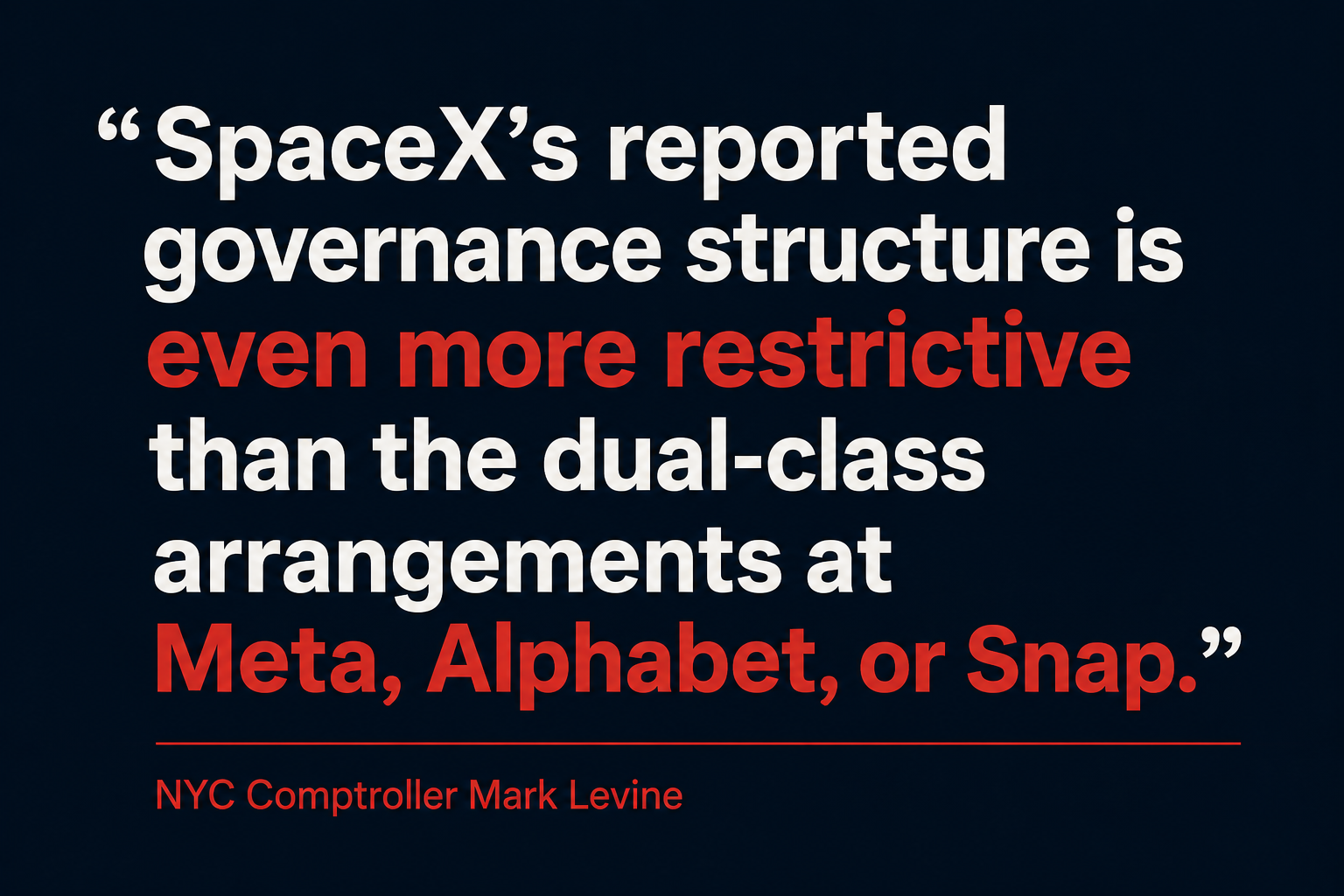

Dear Mr. Musk, Ms. Shotwell, and Mr. Johnsen:We write as the Trustee of the New York State Common Retirement Fund, the investment adviser, custodian, and a trustee of the five New York City public pension systems, and Chief Executive Officer of California Public Employees’ Retirement System, with combined assets under management exceeding $1 trillion, held for millions of working and retired public servants, teachers, firefighters, police officers, nurses, and other beneficiaries whose retirement security depends on the long-term health of the U.S. public capital markets and strong corporate governance.We are writing to express our serious concerns with the reported novel and extreme governance structure and provisions SpaceX is planning to disclose in its registration statement. Public reporting following the Company’s April 1, 2026 confidential submission of its draft registration statement indicates that the proposed governance would constitute the most management-favorable governance structure ever brought to the U.S. public markets at this scale. These reported provisions include perpetual super voting shares, a CEO removal restriction that requires the CEO’s own consent for removal, mandatory arbitration of shareholder claims, controlled company status that has qualifications for exemptions for certain independent board requirements, Texas-law barriers to limit derivative litigation, and concentration of CEO, CTO, and Chair roles in a single individual who simultaneously leads multiple other large-scale companies.The signatories of this letter, like virtually all public pension funds, hold substantial passive allocations indexed to the broad U.S. equity market. If SpaceX is admitted to the major U.S. equity indices following its offering, and the Company’s expected market capitalization makes that admission a near certainty over time, the signatories and their beneficiaries become holders of SpaceX shares.One Share, One VoteThe principle that voting rights should be proportionate to economic interest is considered a hallmark of robust corporate governance. Reports regarding SpaceX’s proposed structure indicate that Class B shares are concentrated in Mr. Musk and a small group of insiders and would carry 10 votes per share, while Class A shares offered to the public only carry one vote per share. Based on this information, Mr. Musk is projected to retain approximately 79 percent of the voting power while holding approximately 42 percent of the equity. Under this structure, public shareholders would acquire the majority of the economic exposure without a corresponding proportional voice in the governance of the company, including the election of directors and/or the potential removal of management.A Board and CEO Governed by ThemselvesSpaceX’s reported governance structure is even more restrictive than the dual-class arrangements at Meta, Alphabet, or Snap. As reported, Mr. Musk could only be removed from the board, or from his positions as CEO and Chair, by a vote of Class B holders – votes he himself controls. Removal of the Company’s most powerful officer would, as a mathematical matter, require his own vote – essentially making him unfireable without his own consent. This level of insulation from accountability is virtually unheard of among any other large U.S. issuer whose governing documents foreclose accountability to public owners on these terms. Compounding this, SpaceX reportedly intends to elect controlled-company status, which would allow it to bypass any requirements for a majority-independent board or for independent compensation and nominating committees, all while Musk simultaneously serves as CEO, CTO and Chair on a nine-person board.Mandatory ArbitrationIt is reported that SpaceX intends to include a provision in its governing documents requiring shareholder claims arising under federal securities laws to be resolved through mandatory binding arbitration. While the SEC reversed its policy in 2025 to allow such clauses, to our knowledge, no major U.S. issuer has previously adopted such a provision for a public offering. Mandatory arbitration eliminates the class-action lawsuit structure essential to remedying widespread harms, keeps corporate law from developing through public court decisions, and shields the Company from the deterrents of sound judicial review. For institutional investors of our size, the inability to participate in or benefit from securities class actions on behalf of beneficiaries or to appeal on the merits, is a meaningful diminution of the legal rights ordinarily attached to a public security.Texas-Law Barriers to Shareholder RightsSpaceX has reincorporated under the new Texas Business Organizations Code. According to reports, the Company intends to leverage Texas law alongside the Company’s charter and bylaws, to effectively increase the procedural hurdles to initiate tender offers, proxy contests, or shareholder proposals. These measures are also expected to complicate the removal of incumbent directors and officers. Furthermore, under the recently enacted Texas law, Texas incorporated public companies may amend their bylaws to require shareholders to hold up to three percent of outstanding stock to maintain standing for a derivative action. At SpaceX’s projected valuation, that 3% threshold would require a shareholder to hold billions of dollars in stock to be able to commence litigation. In practice, this creates nearly insurmountable barriers to accountability where it is likely that only Mr. Musk himself could meet such an ownership requirement. According to analysts, these high thresholds effectively eliminate derivative litigation as a real mechanism for shareholder-led corporate governance accountability.Ongoing Governance ConcernsInvestors evaluating SpaceX’s proposed structure cannot do so in isolation—and must consider it alongside documented oversight challenges in related entities. On December 19, 2025, the Delaware Supreme Court reversed the prior recission of Mr. Musk’s 2018 Tesla compensation package in the Delaware Court of Chancery’s decision in Tornetta v. Musk. Notably, the Delaware Supreme Court did not reach the merits of the lower court’s findings—including that the process was “unfair” and that Mr. Musk exercised “control” over a non-independent board –instead expressly resolving the appeal on the narrower ground that total recission was an improper remedy and noted that the Justices held “varying views on the liability determination.”Following the initial Tornetta decision, Tesla reincorporated from Delaware to Texas, where Tesla shareholders subsequently approved a new performance-based compensation package for Mr. Musk valued at up to approximately $1 trillion at maximum payout, the largest executive compensation arrangement in the history of the public markets. Press reports indicate that the SpaceX board followed a similar pattern in January 2026, reportedly approving a parallel performance-based grant providing for up to 200 million super-voting Class B restricted shares, contingent on reaching a $7.5 trillion valuation and establishing a one-million-person Mars colony, together with an additional tranche of up to 60.4 million super-voting shares, tied to separate valuation targets and the operation of space-based data centers. These awards were reportedly approved without an independent compensation committee process. The pattern, moving compensation outside customary governance checks, relocating to jurisdictions that constrain shareholder remedies, and structurally entrenching the founder against removal, is a through-line that long-term capital is entitled to weigh.Mr. Musk’s regulatory and securities law history also remains material to the governance assessment. In 2018, the U.S. Securities and Exchange Commission charged Mr. Musk with civil securities fraud arising from his “funding secured” tweet about taking Tesla private. Mr. Musk and Tesla each paid $20 million in penalties; Mr. Musk was required to step down as Chair of the Tesla board for at least three years; and the Tesla board was required to implement controls over Mr. Musk’s public communications. The Second Circuit affirmed the enforceability of that consent decree against Mr. Musk’s First Amendment challenge in 2023. In January 2025, the SEC filed a separate civil enforcement action alleging that Mr. Musk failed to timely disclose his beneficial ownership of more than five percent of Twitter common stock in 2022, and underpaid Twitter shareholders by at least $150 million as a result. In May 2026, Elon Musk Revocable Trust reached a proposed $1.5. million settlement, notably the maximum statutory fine for this type of violation, with the SEC to resolve these allegations without admitting or denying wrongdoing. This agreement, which awaits final approval from the court, would result in the dismissal of claims against Mr. Musk personally.Mr. Musk is currently seeking to overturn a March 2026 jury verdict in a separate class-action lawsuit where he was found liable for defrauding Twitter shareholders during the acquisition process. Moreover, there is ongoing litigation around SpaceX’s environmental impacts, and Tesla’s Autopilot safety and ongoing governance battle with OpenAI. These matters bear directly on disclosure discipline and on fiduciary norms. All of this takes on heightened importance in a company whose proposed governance excludes the ordinary mechanisms by which shareholders would otherwise enforce them and as other significant legal actions remain pending.The arrangements reported at SpaceX must also be evaluated against the competing demands on Mr. Musk’s time and attention. Mr. Musk would serve concurrently as CEO, CTO, and Chair of SpaceX while continuing to lead Tesla, X, xAI, the Boring Company, and Neuralink. The simultaneous Tesla and SpaceX compensation packages, each conditioned on extraordinary multi-year valuation and operational milestones, place SpaceX and Tesla in the unusual position of essentially competing against one another for the focused attention of their shared chief executive. Long-term shareholders, under the reported governance structure, will have no independent board majority, no functioning derivative remedy, and no entitlement to true judicial review through which to address the conflicts that this concentration of roles will inevitably produce.Related-Party Entanglement Across the Musk EnterpriseIt has been reported that SpaceX consummated an all-stock acquisition of xAI in February 2026, valuing the combined entity at approximately $1.25 trillion. Furthermore, Tesla reportedly invested $2 billion in SpaceX during the first quarter of 2026; and both companies are allegedly engaged in the joint development the Terafab semiconductor facility. These transactions occurred before SpaceX had a public board, public shareholders, or an independent committee process of the type ordinarily applied to controlling shareholder transactions. The proposed governance structure offers no assurance that future transactions among Mr. Musk’s affiliated entities, including any potential SpaceX-Tesla combination of the kind publicly speculated upon, will be rigorously evaluated by directors independent of Mr. Musk and approved by the uncoerced informed vote of a majority of the unaffiliated public shareholders.We acknowledge SpaceX’s extraordinary technical and commercial achievements, and we recognize the role the Company plays in U.S. national security and commercial space.In fact, precisely because SpaceX is poised to occupy a position of systemic importance in the public markets, and to become, through index inclusion, an unavoidable holding in our portfolios, its governance must at least adhere to the baseline protections upon which long-term institutional capital depends, rather than seeking to diminish them.We respectfully urge SpaceX to reconsider its alleged proposed governance structure prior to filing the S-1. At a minimum, to ensure such strong corporate governance, we believe the offering should:- Adopt a one-share, one-vote structure or, in the alternative, a time-based sunset on super-voting shares of no more than seven years from the IPO;

- Eliminate any provisions conditioning removal of the CEO or Chair on the consent of the officer being removed;

- Ensure a majority-independent board, separate the CEO and Chair roles, and maintain independent compensation, nominating, and audit committees;

- Eliminate any mandatory arbitration provision applicable to shareholder claims or disputes;

- Forgo the Texas three-percent threshold rule for derivative actions; and

- Require all material related-party transactions with Mr. Musk’s other affiliated entities be approved by a committee of independent directors and a non-waivable majority-of-the-minority vote of unaffiliated shareholders.

American Federation of Teachers writes to the US Securities and Exchange Commission

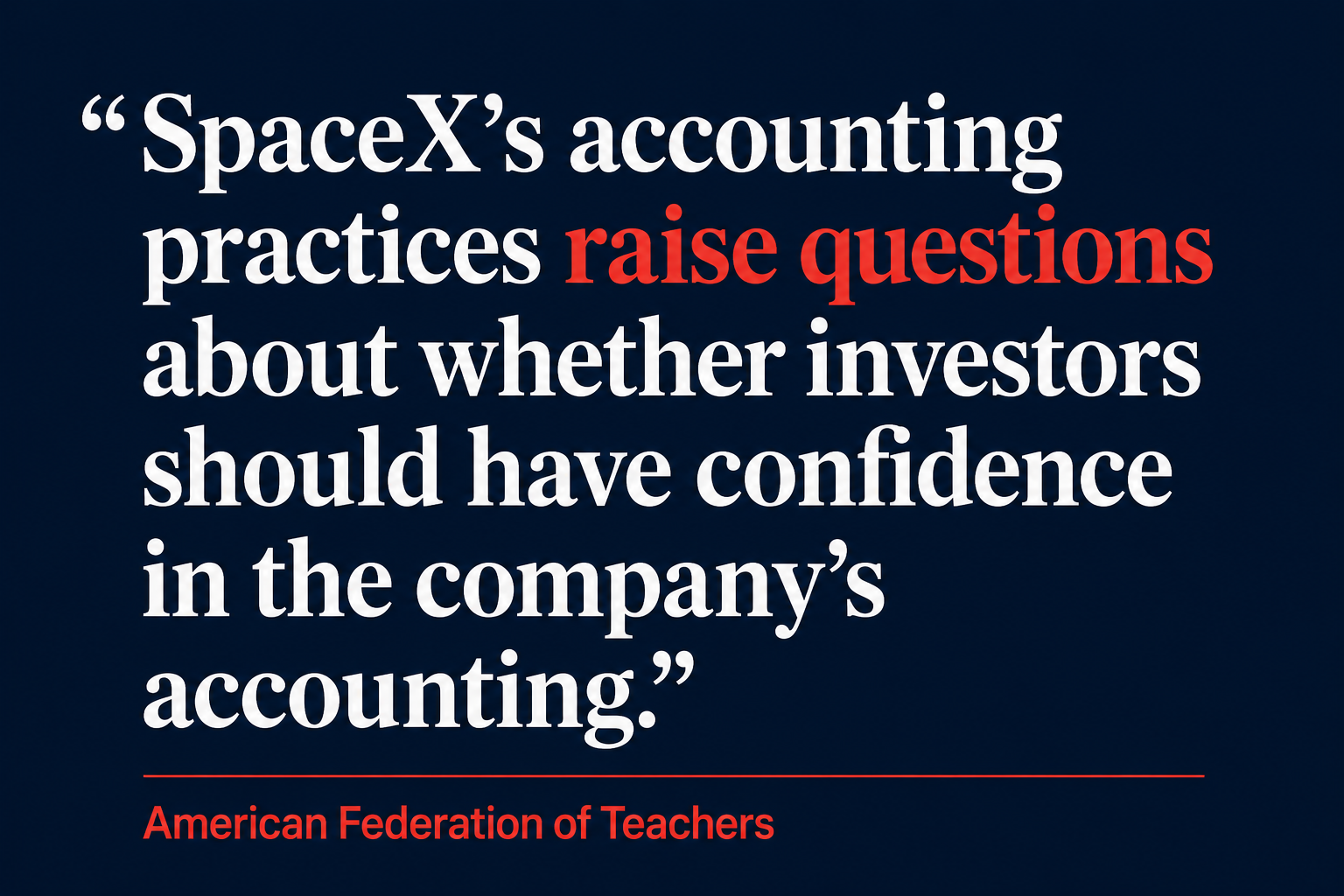

Dear Chairman Atkins,I am writing to you as president of the AFT, on behalf of the 1.8 million education, healthcare and public sector workers we represent. The retirement security for many of these workers relies upon defined-benefit and/or defined-contribution plans, which are exposed to broad swaths of the public equities market. It is with concern for the security of their retirements that I write to you to raise potential issues relating to an initial public offering (IPO) for Space Exploration Technologies Inc. (SpaceX), reportedly under review by the Securities and Exchange Commission.By all indications, the SpaceX IPO will be the largest in U.S. history, surpassing the 2019 Aramco IPO. I have significant concerns about the degree to which this extremely large offering will comply with the securities laws’ requirements concerning full disclosure of material information and fair treatment of investors—both in light of the prior conduct of the SpaceX officers and board and the press accounts of the offering itself. I respectfully request that the commission look into a series of specific significant issues associated with the SpaceX offering as part of the SEC review process. These issues are cross jurisdictional within the commission—affecting the work of Corporation Finance, Trading and Markets, Investment Management, the Chief Accountant’s Office, and are thus properly your responsibility as chairman.Our concerns are driven by the potential impact of the IPO on the 1.8 million education and healthcare professionals represented by the AFT. Our members participate in retirement and other benefit funds with approximately $3 trillion in assets, and many of our members also invest in the capital markets as individuals. The breadth of the disclosure, accounting and governance issues associated with the SpaceX offering will significantly affect AFT members and their benefit funds, given the size of the offering and the degree to which it is being marketed to retail investors, who are estimated to be receiving 30 percent of the offering. We are also concerned about how this offering is being treated by the listing exchange Nasdaq—reportedly also being considered by S&P—that effectively means our members will be compelled to invest in SpaceX in a manner disproportionate to its real market capitalization.1To address these concerns, I ask that the commission subject the offering to scrutiny in the following areas:1st Disclosure of risk factors around the core issue of how and when SpaceX will generate sufficient earnings to support its current reported offering price of approximately 200 times cashflows—Such risk factors should include business risk, including but not limited to the risk of competition, total addressable markets for the products, science and engineering risk, and political risk. Business plans that depend on currently nonexistent or speculative technologies must be disclosed as such.2nd Accounting Practices. There are extensive press accounts describing aggressive and possibly non-GAAP accounting practices at SpaceX—particularly in relation to revenue recognition, related party transactions that have driven the company’s private valuations to date, capitalization of expenses, and depreciation of capital assets. Both SpaceX’s internal financial accounting practices and its independent auditor’s audit of those practices require the most rigorous and thoroughgoing review by the commission prior to approving the financial statement portion of SpaceX’s offering documents.3rd Governance. Three of four known pre-offering board members at SpaceX are close personal friends of Elon Musk, and investors in other companies owned by Musk and his brother, Kimbal. Particularly in light of the reported dual-class share structure and limitations on actionable shareholder rights under recent Texas state securities law changes, a truly independent board is critical.2The commission must ensure that the disclosures associated with SpaceX’s corporate governance are complete, particularly with respect to the background and qualifications of SpaceX’s directors. The commission should be working with NASDAQ to ensure that SpaceX is in compliance with both the provisions of the Sarbanes-Oxley Act and NASDAQ”s listing standards with respect to director expertise and independence.While not directly related to the IPO, the SEC should examine the question of forced investment. Due to changes to indexes made in advance of the SpaceX IPO, retail investors holding broad index funds will be forced to invest in SpaceX just days after the IPO. NASDAQ’s “fast entry” rule enacted at the end of March and taking effect May 1, eliminated the float requirement, and dropped the waiting period for newly listed securities for companies. This rule change allows companies in the top 40 of the NASDAQ 100 to be included in indexes after just 15 days, rather than three months, a timeframe we fear is woefully insufficient for the market to accurately price the potentially significant risks inherent in the concerns outlined above. In addition, NASDAQ has changed its rules so that the weight given to SpaceX in the index will be based on the company’s total implied market capitalization, not the actual number of shares available to the public. This will magnify forced holdings in SpaceX by a factor of 10, in apparent disregard for the financial logic of indexing. All of these changes should be strictly scrutinized by the Divisions of Trading and Markets and Investment Management.Again, it is important to re-emphasize why from an investor protection perspective the commission should engage in extraordinary scrutiny of the SpaceX initial public offering. SpaceX is not a startup; it is 24 years old, has been active in its various component businesses for years and in some cases more than a decade, and has substantial revenues. Nonetheless, the reported valuation contemplated in the IPO appears unsupported by the company’s fundamentals and based on highly speculative future revenue projections based on key operational milestones that may never be met, let alone in the immediate future.At a reported target valuation of $1.75 trillion, SpaceX is angling to be the largest IPO in history. But with revenues of only $18.5 billion, SpaceX would be trading at roughly 95x trailing revenue. At peak, Nvidia traded at a revenue multiple of 40-50 times. SpaceX would also be valued at least 270 times consolidated adjusted EBITDA, more than twice that of Palantir and 16 times the public company average.4 Assuming the entirety of the firm’s reported $18.5 billion revenues in 2025 came from sales, SpaceX would have a price-to-sales ratio of 95 times. For comparison, Twitter’s 2013 IPO shares were priced at 12.4 times sales. Finally, despite artistic accounting, press accounts report that from a GAAP earnings perspective, SpaceX has never been profitable.Public reporting about SpaceX’s accounting practices also raise questions about whether investors should have confidence in the company’s accounting. A 2024 article in Bloomberg claims that individuals “familiar with the finances” of SpaceX subsidiary Starlink have described the company’s accounting as “more of an art than a science.”5 However, in a development reminiscent of the analyst scandals during the dot-com bubble, there is reason to doubt there will be independent sell-side research into this offering, given that 21 banks reportedly have some role in underwriting, raising the concern of potential widespread conflicts. This makes it even more important that the SEC thoroughly review this proposed listing.Finally, governance and board composition play a larger role in SpaceX than at most public companies because SpaceX: (1) is reported to be contemplating a dual-class voting structure that would weaken direct shareholder oversight and {2) derives material revenues from sensitive activities on behalf of the intelligence community, the National Reconnaissance Office and NASA.So, in addition to general business and financial risk associated with governance issues and compliance with the Sarbanes-Oxley Act, NASDAQ listing rules and state law, it would appear to be material to an investment decision to know whether there were facts about the companies’ directors that could endanger those customer relationships or otherwise jeopardize SpaceX’s ability to operate, in light of its customer concentration with government entities.To take two examples of partially publicly available information, according to an FBI report from April 3, 2025, SpaceX board member Steve Jurvetson is reportedly being blackmailed by former Draper Fisher Jurvetson staffer Frank Moyle Creer, over activity that reportedly occurred at a “a private, high-end, high-initiation-fee sex/swingers club in Los Angeles and Northern California called ‘Sanctum.’” Jurvetson left Draper Fisher Jurvetson after accusations surfaced that he had acted inappropriately toward women at the firm, allegations that Jurvetson has publicly denied.A second board member, Antonio Gracias, oversaw the Social Security Administration as a representative of the Department of Government Efficiency, at a time when Social Security data was unlawfully transferred to a conservative social welfare organization. A federal judge has ordered discovery into this transfer, and the SSA has referred two unnamed DOGE staffers for potential Hatch Act violations in connection with the transfer. The commission should insist on complete disclosure of all material facts about these two and all other directors of SpaceX in the S-1.In conclusion, the SpaceX IPO is no ordinary offering. Its size, pricing, listing process and governance background raise numerous cautions relating to the commission’s investor protection mandate. I urge the SEC to thoroughly examine the S-1 and require SpaceX, its independent auditor, NASDAQ, and NASDAQ index fund managers to fully comply with all of the provisions of the securities laws affecting this offering. AFT members, our benefit funds and all other investors’ interests must be fully protected, as they are entitled to be under our nation’s securities laws.My staff and I are available to the commission if we can be of any further assistance in this matter. Please email AFT’s Center for Workers’ Capital at cwc@aft.org if you have any questions or would like to discuss our concerns further. Thank you for your attention.Sincerely,Randi WeingartenPresident